Get a quote in

Get a quote in

Expert UK team

Expert UK team

Van Insurance for Over 60s: FAQs & Key Insights

Van insurance for drivers over 60 is designed to reflect the typically lower-risk profile of older motorists. These policies often provide more favourable pricing and can come with fewer restrictions compared to younger age brackets. Whether you are semi-retired, retired, or still using your van for business, insurers assess your experience and driving history when calculating premiums.

Insurance pricing is never based on age alone. Risk assessments usually include:

- Driver factors: age, driving record, claims history, profession, location.

- Vehicle factors: age, make/model, modifications, safety and security features.

- Usage factors: annual mileage, purpose (social, domestic, pleasure or business), times of day driven.

For over 60s, these combined factors can result in meaningful discounts, especially if paired with a long no-claims record.

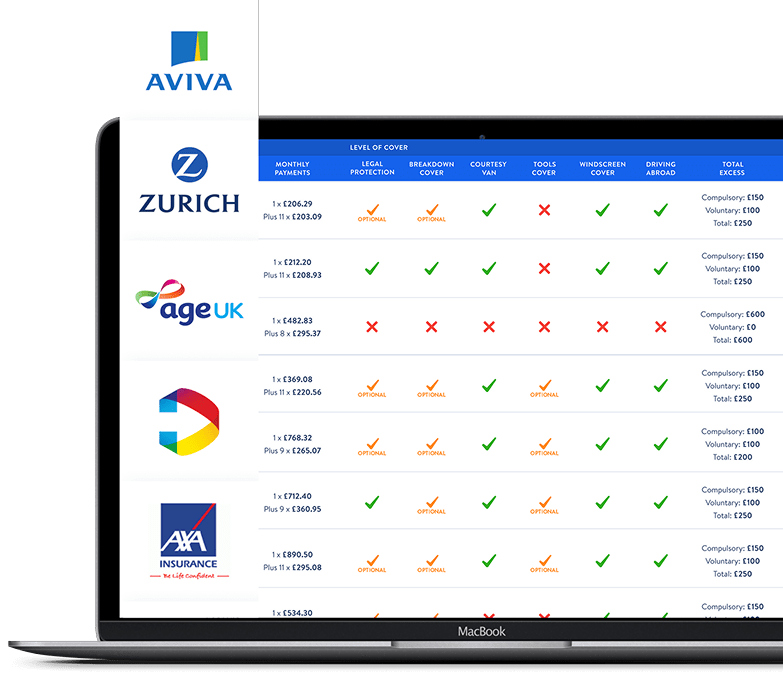

Many drivers in this bracket select additional protection for peace of mind, such as:

- Windscreen cover

- Breakdown recovery

- Tool protection

- Personal belongings and contents cover

- Public liability (if still using the van for work)

- Third Party Only – minimum legal requirement.

- Third Party, Fire and Theft (TPFT) – adds extra protection for common risks.

- Comprehensive – usually still competitively priced for over 60s, offering the widest cover.

- Install security systems or trackers to reduce theft risk.

- Limit cover to personal use only if no longer working.

- Store the van securely overnight (garage or driveway preferred).

- Protect your no-claims discount by avoiding small claims.

- Adjust voluntary excess to balance affordability and protection.

Insurers use actuarial data and historical claims records to set prices. Drivers over 60 are statistically:

- Less likely to engage in risky behaviour such as speeding or late-night driving.

- More experienced, with decades of driving history to demonstrate competence.

- Lower frequency claimants, reducing expected loss ratios for insurers.

This translates into lower base premiums and often access to higher levels of cover at affordable prices.

While drivers in their early 60s often enjoy reduced premiums, this trend can reverse in the late sixties (typically 68+). This is particularly true for older drivers with adverse driving histories (claims, convictions, cancelled policies). The main reasons are:

- Reduced competition: some insurers choose not to provide quotes over certain ages.

- Specialist markets: niche insurers who focus on higher-risk profiles (e.g. haulage, multiple claims, previous cancellations) are usually more selective, with age being one factor in deciding whether to offer terms. This shrinking pool of providers can lead to higher average premiums.

Yes. Age does not exclude business use, but premiums will be based on the type of work, mileage, and vehicle.

Some insurers may have stricter acceptance criteria once drivers reach 75 or 80. Premiums may also begin to rise again from around age 68 due to reduced competition in the market.

Not for standard policies. However, you must declare any medical conditions to the DVLA, and failing to do so can invalidate insurance.

Van insurance for over 60s is usually more affordable thanks to lower risk profiles and long driving histories. However, premiums may rise again for older drivers approaching 70, particularly those with adverse records, as fewer insurers compete for this business. The key is to compare annually, take advantage of age-related discounts where available, and consider add-ons that provide tailored protection such as breakdown recovery or contents cover.