Get a quote in

Get a quote in

Expert UK team

Expert UK team

Under 25 Van Insurance: FAQs & Key Insights

Under 25 van insurance is designed for younger drivers who face higher premiums due to limited driving experience and higher claim frequency in this age group. Policies can provide the same cover options as any other driver, but the pricing and conditions are often stricter.

- Licence tenure: most drivers under 25 have only held a full UK licence for a few years, giving insurers less driving history to assess.

- Claim statistics: this age group statistically has a higher likelihood of accidents, which insurers factor into pricing.

- Limited no-claims bonus (NCB): younger drivers are often just starting to build NCB, if at all.

- Restricted insurer panel: many underwriters simply do not quote below certain ages (commonly 21, 23 or 25), which reduces supply and pushes up prices.

- Compulsory excess: under-25s often face higher compulsory excesses as part of the policy.

Many drivers under 25 have only recently moved from being named drivers on a parent’s or employer’s policy to holding a policy in their own name. Starting earlier means paying more, but it also allows you to begin building your own NCB sooner. For some, it makes financial sense to wait until 21 or 25 when prices fall and more insurers are available.

Some insurers specialise in providing cover for young drivers with higher risks — such as those with no NCB, recent claims, or convictions. These underwriters often open up at 21 or 23, but true breadth of market only emerges once you pass 25. This means under-25s may find fewer options, higher prices, and stricter terms.

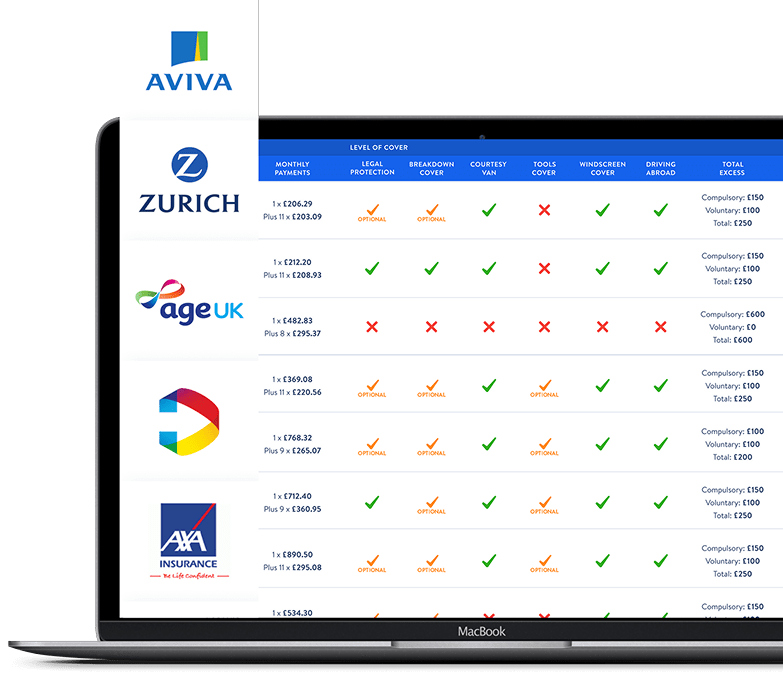

- Third Party Only – meets the legal minimum; protects others, not your van.

- Third Party, Fire and Theft (TPFT) – adds fire and theft cover for your own van.

- Comprehensive – covers your van as well as third parties, even in at-fault accidents. Comprehensive is often priced more competitively than TPFT for younger drivers because it attracts more risk-averse profiles.

- Windscreen and glass repair

- Courtesy van during repairs

- UK & European breakdown cover

- Legal expenses cover

- Personal injury protection

- Telematics (black box) cover — sometimes required for younger drivers

- Take an advanced driving course

- Choose a van with a smaller engine and lower insurance group.

- Avoid unnecessary modifications.

- Park securely overnight.

- Keep your licence clean — even a single conviction can have a big impact at this age.

- Build NCB early if affordable, but weigh against the cost of holding your own policy too soon.

- “Comprehensive cover is always more expensive.” Not true — for under-25s, Comprehensive can sometimes be cheaper than TPFT.

- “Named driver discounts last forever.” Once you need your own policy, named driver history rarely carries over; only your policyholder NCB matters.

- “Non-fault claims don’t matter.” Even non-fault or “notification only” claims can influence insurer pricing.

Insurers regulated by the FCA require full disclosure of age, claims history, and intended use. Non-disclosure — such as failing to mention business use, modifications, or previous claims — can invalidate a policy or lead to a claim being refused.

- Under 21: very few insurers quote; very high premiums.

- Under 25: more options, but still higher risk pool, with limited specialist markets.

- Over 25: broader insurer access, lower compulsory excess, more competitive pricing.

Insurers price based on risk. Younger drivers are statistically more likely to have accidents and usually have less driving history or NCB, which increases premiums.

Yes, but options may be limited. Some insurers will only offer carriage of own goods at 21+, while courier or hire and reward cover can be expensive when under 25.

Many drivers see prices improve after 21, 23, and again at 25, as more insurers are willing to provide quotes and experience builds up.