Get a quote in

Get a quote in

Expert UK team

Expert UK team

Over 25 Van Insurance: FAQs & Key Insights

Over 25 van insurance is designed for drivers aged 25 and above who typically present a lower risk than younger drivers. Turning 25 does not automatically reduce your premium, but many drivers see improved pricing because of the risk and market factors below.

- Licence tenure: many 25-year-olds have held a full UK licence for longer, signalling more experience.

- Clean driving history: there is more time to build claim-free years.

- No-claims bonus (NCB): by this age many drivers have accumulated several years of NCB.

- Broader insurer panel: more underwriters are willing to quote at 25+, which increases competition and can bring prices down.

- Fewer product restrictions: some schemes that are closed to under-25s open up at 25, including lower compulsory excesses or wider cover options.

Pricing always depends on multiple factors, including vehicle, postcode, occupation, mileage and claims. These are general patterns, not guarantees.

Many drivers aged 25 and over will already have been policyholders for several years and will have

begun building

their NCB. Those who have had to make claims may have seen this reduced, as many insurers only allow

NCB protection

once four or more years have been accumulated.

At this stage, a wider range of specialist underwriters may also become available. Many of these

providers only

begin quoting from age 23 upwards and often target specific risk profiles — such as drivers with low

or interrupted

NCB, multiple claims, or past convictions. For drivers in these categories, reaching 25 can open up

new markets and

policy options that were previously unavailable.

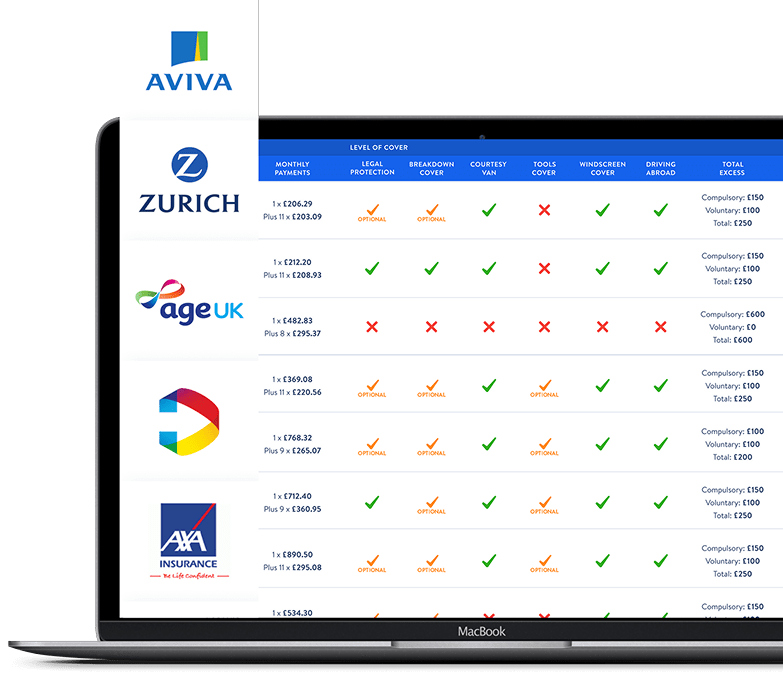

- Third Party Only – meets the legal minimum. No cover for your own van.

- Third Party, Fire and Theft (TPFT) – adds theft and fire cover for your van

- Comprehensive – includes accidental damage to your own van as well as full third-party protection. On some vehicles Comprehensive can be competitively priced versus TPFT.

- Windscreen and glass cover

- Courtesy van while yours is off the road

- UK and European breakdown cover

- Legal expenses cover

- Tools or goods in transit cover for business users

- Protected no-claims discount, where eligible

- Choose a van in a lower insurance group and avoid unnecessary modifications.

- Keep annual mileage realistic and as low as practical.

- Park in secure locations overnight and consider approved alarms, immobilisers or trackers.

- Maintain a clean licence and claims record to continue building NCB.

- Consider named-driver policies rather than any-driver if only a few people use the van.

- “Age alone makes it cheap.” Age is one factor. Pricing also reflects claims history, NCB, vehicle, usage and location.

- “Non-fault claims do not matter.” Even non-fault or notification-only incidents can influence pricing.

- “Business use is automatic.” You must disclose the correct class of use. Carrying tools, visiting multiple sites or doing deliveries usually requires business classifications such as carriage of own goods or hire and reward.

Insurers, under FCA oversight, expect accurate disclosure of driver details and vehicle use. Mis-stating class of use, omitting claims or not declaring modifications can lead to cover being declined or a claim being refused.

- 21+: supply of quoting insurers improves versus under-21, early NCB building phase.

- 25+: broader panel access, specialist markets open, more cover options.

- 30+: risk often stabilises further for many profiles, subject to driving record and vehicle type.

Not always. Many drivers see improved prices at 25 due to experience and increased insurer competition, but your premium still depends on your claims record, NCB, van, postcode and usage.

Yes. Most insurers will consider business use at 25+, including carriage of own goods. Courier or hire and reward cover may have additional criteria.

It can. Insurers consider the full incident history, including non-fault and notification-only claims, when assessing future risk.

Protected NCB can preserve your discount step, but base rates may still change after a claim. It protects the discount, not the underlying premium.