Get a quote in

Get a quote in

Expert UK team

Expert UK team

Commercial Van Insurance: FAQs & Key Insights

Commercial van insurance is a policy required for vehicles that are classified as commercial, regardless of how they are used.

- Even if a van is driven only for social, domestic and pleasure purposes, a commercial policy may still be necessary because of the vehicle type

- When used for work, such as carrying goods, making deliveries or transporting tools, the policy also accounts for business-related risks.

For example:

- Certain versions of the Land Rover Defender,, such as hardtops or pick-ups, are registered as N1 light commercial vehicles even if they are driven privately. These cannot be insured as cars if they are classified as commercial.

- The Ineos Grenadier Commercial is also classed as an N1 vehicle, which means a commercial policy is required even though it looks like a passenger car.

You will usually need commercial van insurance if you:

- Own a vehicle that is classified as commercial, even if you do not use it for work.

- Use your van for deliveries, also known as hire and reward.

- Carry tools, stock or equipment for your trade.

- Operate a fleet of vans with multiple drivers.

Using private cover for a vehicle that is classified as commercial can invalidate your insurance and leave you non-compliant with the Road Traffic Act 1988.

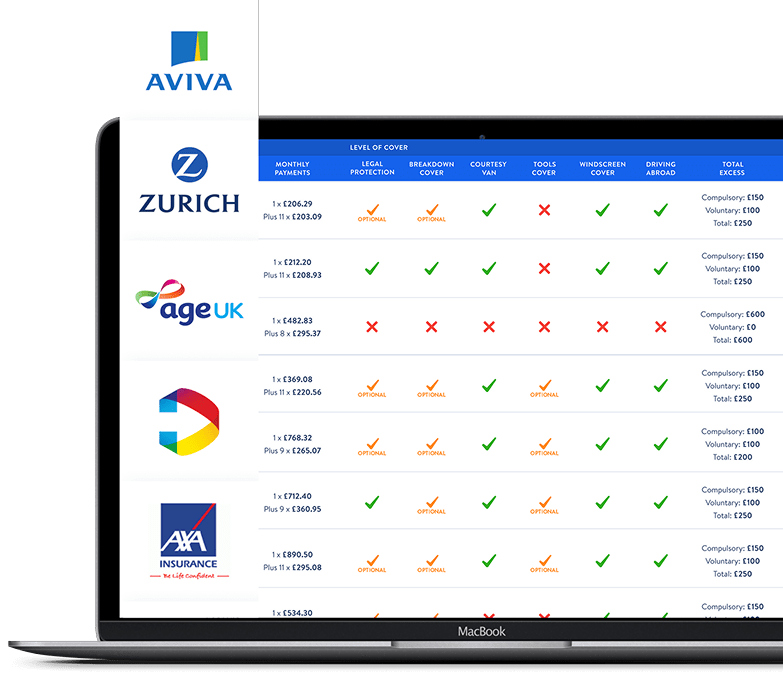

| Cover Type | What it Includes | When to Use |

|---|---|---|

| Third Party Only | Covers damage to others and their property. | The legal minimum for any commercial vehicle. |

| Third Party, Fire & Theft (TPFT) | Adds protection against fire damage and theft. | Suitable for lower-value vans where theft is a risk. |

| Comprehensive | Covers your van as well as third parties, fire and theft. | Best for higher-value vans or where business continuity depends on the vehicle. |

- Carriage of Own Goods – for example, a tradesperson carrying their tools.

- Hire and reward – for example, couriers or delivery drivers transporting items for customers.

- Haulage – long-distance or larger-goods transport.

Even if you drive the van purely for private purposes, insurers will still classify the policy as commercial if the vehicle is registered that way.

Often, but not always. Premiums depend on driver history, usage type, storage postcode and the specific vehicle.

Not if the vehicle is classified as a commercial model. Even for purely social or leisure driving, insurers will require a commercial policy.

Yes. Certain vehicles that resemble cars, such as some Defender hardtops or the Ineos Grenadier Commercial, are classified as commercial and must therefore be insured on that basis.

If you say your van is for private use when it is being used commercially, or if you insure a commercial-classified vehicle on a private policy, claims may be denied, and the policy may be cancelled.

All commercial van insurance sold in the UK must comply with FCA regulations and the Road Traffic Act 1988. The vehicle’s classification, not just its use, determines whether a commercial policy is required.

Commercial van insurance is not only about how you use the vehicle. It is heavily determined by whether the van, or an SUV-style vehicle such as certain Defenders or the Ineos Grenadier, is classified as commercial. This means that even private-only drivers may still need commercial cover. Choosing the right type of policy, from Third Party Only through to Comprehensive, with add-ons such as public liability or goods in transit, ensures you remain compliant, protected and appropriately covered.