Get a quote in

Get a quote in

Expert UK team

Expert UK team

Third Party Van Insurance: FAQs & Key Insights

1. What Is Third Party Van Insurance?

Third party van insurance is the minimum level of cover required by law in the UK. It protects other people and their property if you are responsible for an accident. Your own van is not covered, meaning any repairs or replacement costs would fall to you.

2. Who Is It Suited For?

- Drivers of older or lower-value vans who want legal cover but do not wish to pay higher premiums

- Experienced drivers with a clean claims history

- Low-mileage van users who accept the risk of no cover for their own vehicle

- Cost-conscious drivers needing the most basic protection

3. What Does It Cover?

- Injury to third parties (drivers, passengers, pedestrians)

- Damage to other vehicles or property

- Legal costs arising from third-party claims

4. Common Misconceptions

- Third Party Only is rarely the cheapest option. Because so few insurers offer it, competition is limited and premiums can actually be higher than TPFT. Historically, insurers found that drivers choosing TPO were more likely to be involved in accidents, which has kept prices elevated.

- Expensive vs cheap vehicles. Insurers often expect a driver of a high-value van to be more cautious, while drivers of lower-value vans have been statistically riskier. This counterintuitive logic helps explain why high levels of cover is sometimes cheaper than TPO.

- Limited protection. TPO does not cover your own van, its contents, or tools. However, tools cover can still be added separately.

- Unsuitable for business-critical vehicles. If your van is essential to your trade, the financial risk of being left uncovered for your own vehicle usually outweighs the savings.

5. Add-Ons Still Available

Although Third Party is basic, insurers may allow certain extras, such as:

- Windscreen cover

- Breakdown recovery

- Tool protection

- Legal expenses insurance

- Public liability (for business use)

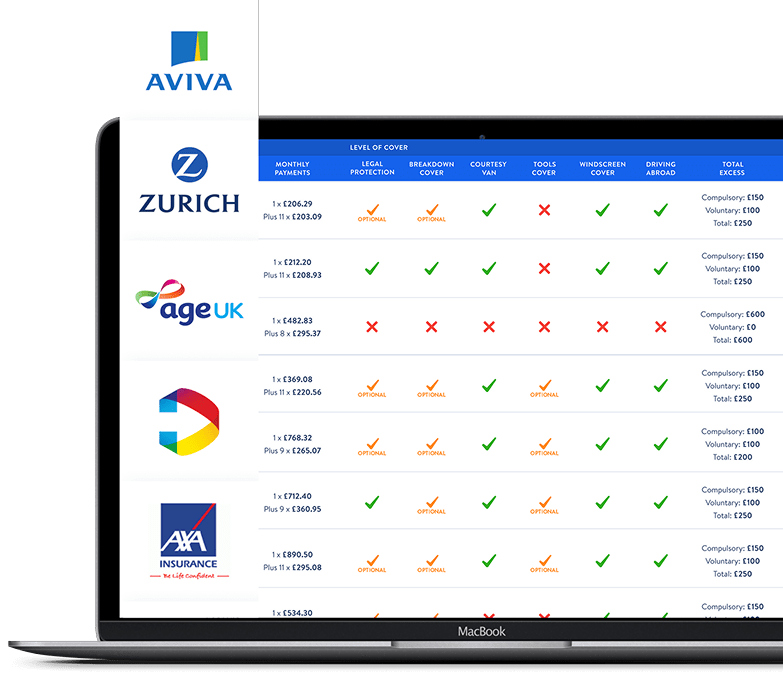

6. Comparison With Other Cover Types

- Third Party Only (TPO) – legal minimum, least protection, often less widely available.

- Third Party, Fire & Theft (TPFT) – adds protection if your van is stolen or damaged by fire.

- Comprehensive – covers everything above plus accidental damage to your own van.

7. How to Lower Your Premium

- Restrict the policy to experienced drivers

- Park securely overnight (garage or locked compound)

- Limit mileage and avoid unnecessary modifications

- Maintain a no-claims discount

- Compare policies annually to ensure best value

8. Important to Note

- Some insurers will only offer TPFT or Comprehensive, particularly if your van is high-value or very old.

- Compulsory excess levels may differ depending on whether you choose TPO, TPFT, or Comprehensive.

- Always check whether add-ons are available, as they are sometimes restricted on Third Party policies.